Why a $270K Nest Egg Doesn’t Cut It

What Happens When Your Retirement Meets Real Life?

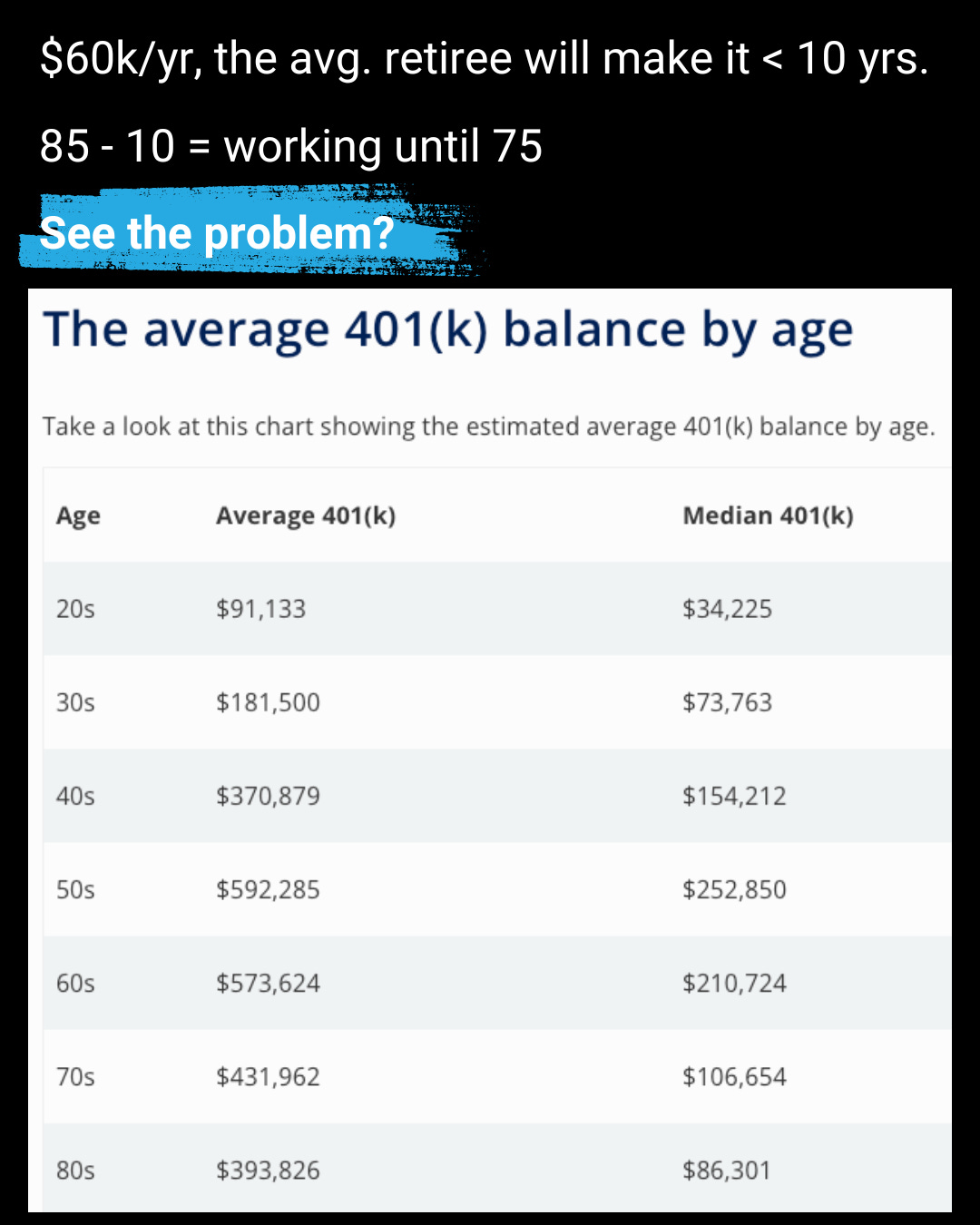

We’re told that a 401(k) and a decent savings account will carry us through retirement.

But let’s do the math:

Rent → $2,000

Food → $500

Utilities → $200

Medical → $500

Life → $500

That’s $3,700 a month, or $44,400 per year.

If you retire with the median nest egg of $270K, you’re covered for just six years. Then what?

The Myth of the 401(k) Safety Net

A 401(k) isn’t a bad tool—but it was never meant to be the entire plan.

It doesn’t give you:

Monthly income

Tax advantages

Asset control

The flexibility to adapt to market changes

And it certainly doesn’t keep up with inflation, healthcare spikes, or rising housing costs.

Wealthy people know this.

That’s why they don’t just chase account balances.

They build cash flow.

🏠 Interested in starting or growing your real estate portfolio? Join a community of changemakers investing to build wealth and create impact.

The Real Strategy: Build Cash Flow

If you want to retire (and stay retired), you need income that shows up every month.

That comes from:

Business ownership

Cash-flowing real estate

Multiple income streams

Tax-advantaged investments

Real estate offers more than just appreciation—it brings tools like:

Depreciation (to lower taxable income)

1031 exchanges (to defer taxes on gains)

Bonus depreciation (now back under the new tax bill)

Greater control over your asset and outcome

Why This Matters Now

The new tax bill just shifted the game for investors:

100% bonus depreciation is back

SALT deduction cap raised

Translation: Investors keep more of what they earn, faster

The rules of the game are changing—and real estate is winning again.

A 401(k) is a tool.

But cash flow is the plan.

That’s why I invest in real estate—and help others do the same.

Because real wealth isn’t what’s in the account.

It’s what shows up every month, even when you don’t.

Until next time,

Jon

Thanks for reading Drops of Change! Subscribe for free to receive new posts and support my work.